Time for Ministers to intervene on Investment Trusts, as FCA has failed to achieve change

- Emergency intervention to protect UK investment trusts from flawed Regulations could turbocharge UK markets and growth while boosting investor returns.

- Ministers must no longer leave it to the FCA to keep dithering and consulting while their misleading rules destroy investor support on a false premise.

- UK-listed investment trusts help democratise investing for retail and institutional investors in long-term, less liquid assets such as infrastructure, growth businesses and renewable energy.

Ministers must no longer leave it to the FCA to keep dithering and consulting – FCA was asked to take urgent action, but nothing has changed: The Chancellor, in his Autumn Statement, asked the FCA to take action to remedy the problem of misapplied charges disclosure regulations which force investors to sell UK-listed investment trusts, driving pension funds to buy overseas investment companies instead. Since then, however, nothing has changed and the exodus of capital from the Investment Companies sector has accelerated. This selling pressure and loss of investor support is based on a false premise, created by Regulations that were meant to protect consumers but actually do the opposite. Ministers must no longer leave it to the FCA to keep dithering and consulting. Having recognised that the rules guiding charges disclosures for UK listed investment companies are misleading investors, the much-needed urgent change has not materialised. Action is needed now.

UK Investment Trusts are being starved of capital as regulations require them to misrepresent investor costs: UK investment trusts are a long-standing British success story. For over 150 years, they have offered access to ready-made portfolios which most investors could not put together or manage themselves. The closed-ended investment structure is ideally suited to long-term institutional investment in illiquid assets, and offers exposure to a wide range of environmental and social investments. But the sector has been undermined in recent years by charges disclosure rules have been misapplied to investment trusts, forcing these companies to show misleading information to investors, and exaggerate the costs of holding their shares. This has culminated in waves of selling, lack of buyers, unwarranted large discounts to net asset value and share price weakness that has stopped capital raising for vital growth sectors as UK investment companies suffer an exodus of capital from institutions and wealth managers.

Emergency intervention could help protect this important sector, which makes up over 30% of FTSE250 and supports vital economic growth areas: Intervention is needed now, to stem the tide of selling and start to revive the investment trust sector. This will also boost UK financial markets as a whole, since investment companies make up well over 30% of the FTSE250 and, therefore, UK indices have been dragged down along with the investment trusts themselves.

Regulations derived from the EU have been imposed uniquely on UK-listed investment trusts, driving investors to sell on a false premise: The market dislocation in investment trusts is being driven in large measure by a unique application of retained EU law which differs from the way the same law is applied in every EU member state. The perverse British interpretation of EU regulations has made UK-listed investment companies appear misleadingly expensive for investors to hold, driving an exodus of capital from institutions and retail investors, as retail investor platforms have removed these companies from their platforms on a false premise.

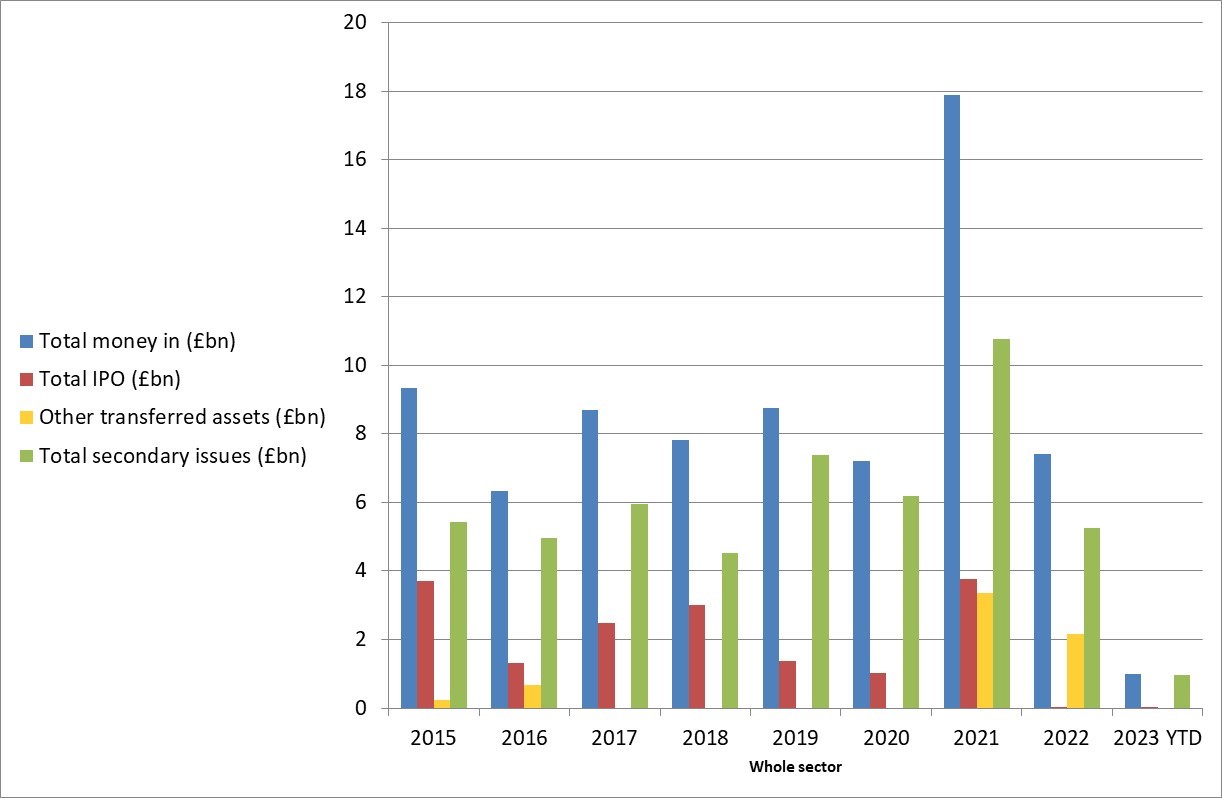

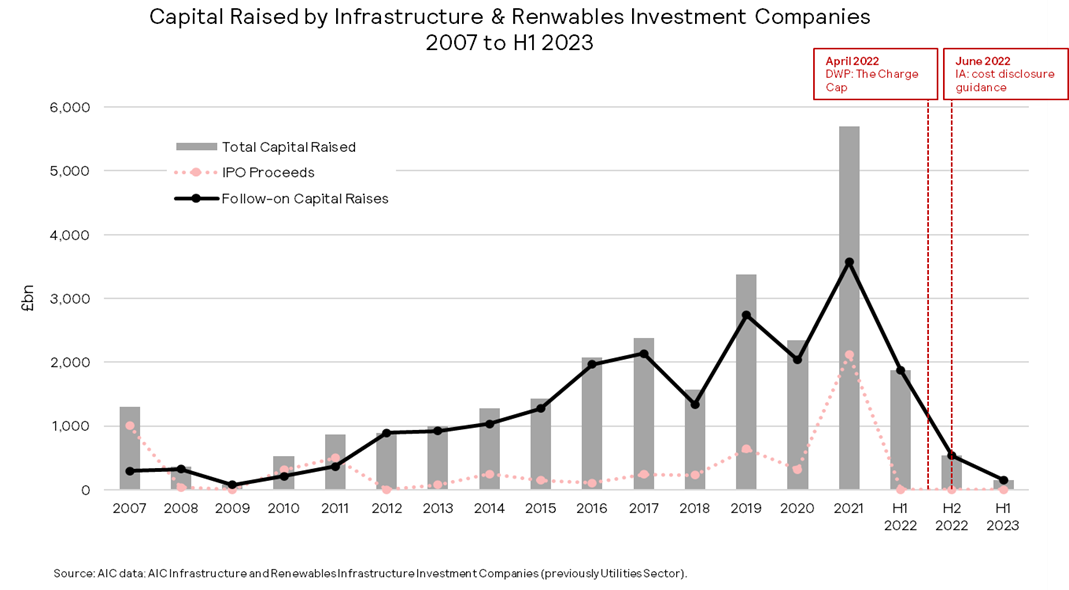

Funding has dried up as investors use non-UK listed investments or riskier individual shares instead: Wealth Managers, funds of funds and pension investors are being obliged by UK Regulators to report operating expenses (that are of course properly reported in financial statements) to investors as though they were part of their own fund management fees. They are required to double count the cost of investing. And rather than do that they simply sell the shares. The consequent flight of capital is a disaster for the very assets the government wants the private sector and pension funds to support. No other stock exchange in the world obliges shareholders in any listed company to report the costs of a listed investee company as though they were part of their own fund management charges. The impact on funding is clear from the charts below:

Unwarranted discounts to Net Asset Value have opened up, as investors are switching overseas, where the UK disclosure rules do not apply. Funding for UK-listed investment trusts has dried up, depriving the economy of an important source of growth capital for the very areas which Government would like pension funds and other investors to support. Most investment trusts invest in real assets, including vital infrastructure projects such as schools, motorways, affordable housing, police and fire stations, and NHS hospitals in the UK, which can deliver strong long-term income, offering good dividend yields over time.

Unwarranted discounts to Net Asset Value have opened up, as investors are switching overseas, where the UK disclosure rules do not apply. Funding for UK-listed investment trusts has dried up, depriving the economy of an important source of growth capital for the very areas which Government would like pension funds and other investors to support. Most investment trusts invest in real assets, including vital infrastructure projects such as schools, motorways, affordable housing, police and fire stations, and NHS hospitals in the UK, which can deliver strong long-term income, offering good dividend yields over time.

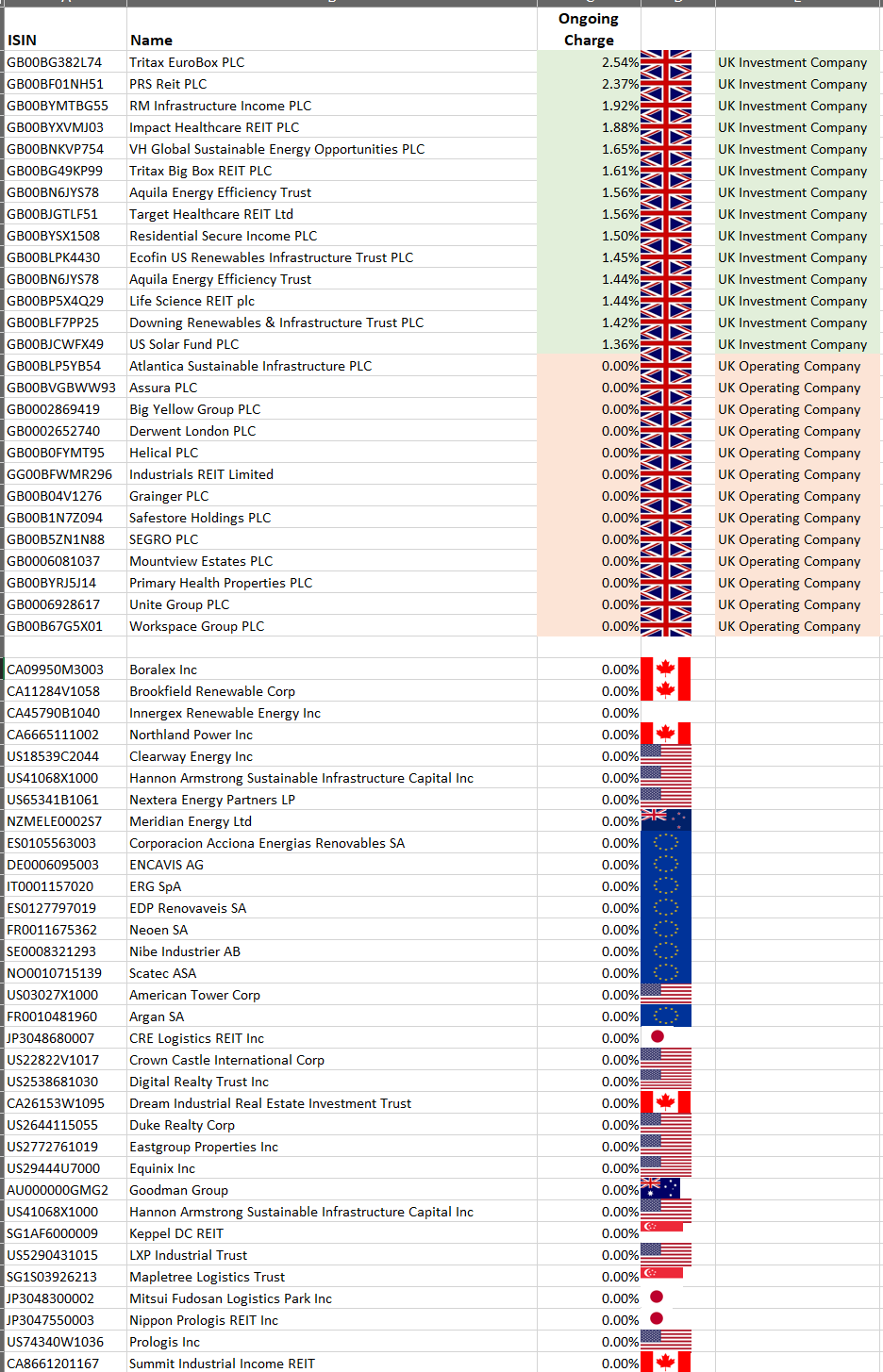

The UK is choosing to shoot itself in the foot, as regulations make UK listed investment trusts look uniquely unattractive with all global competitors: Investors are switching out of UK markets needlessly, which is depriving consumers of dependable dividend paying investments, and denying them access to ready-made portfolios which could add diversification and improve risk-adjusted long-term returns. Ironically, the rules were imposed in the name of consumer protection, yet they have achieved the exact opposite. Ending these flawed consumer cost disclosures, will help properly informed consumers make better decisions and bring back stability to the precious investment trust sector and harness the power of UK pensions, ISAs and retail investments to support Britain better. The uniqueness of the misleading charges reporting by only UK listed investment companies is shown clearly in the table below. No other country tells investors that the investor will bear a direct ongoing charge for holding their company’s shares, when that is simply not the case. These so-called ongoing investor charges are not costs to the investor directly, they are operating expenses of each company and are disclosed as such. Only UK investment companies have figures shown as ‘ongoing charges’, making them uniquely unattractive for investors when compared with all global competitors.

COMPARISON OF UK & NON-UK LISTED INVESTMENT COMPANIES – OFFICIAL EMT TABLES

ALL NON-UK LISTED COMPANIES SHOW CORRECTLY THAT THE INVESTOR IS NOT DIRECTLY CHARGED

USE OF EMT TABLES NEEDS TO URGENTLY CHANGE TO END THESE MISLEADING DISCLOSURES

Ongoing charges figures for all non-UK listed investment companies are published as zero in the EMT.

The current system misleads consumers and undermines the remit set by Parliament for the FCA: The FCA’s objectives include protecting the integrity of UK financial markets – these charges disclosures have decimated the investment trusts sector. FCA must ensure international competitiveness for our firms – again these charges disclosure have made the UK uniquely uncompetitive. The FCA is meant to support the economy and sustainable growth – but by driving investors away from our listed investment companies, these rules mean vital areas of the economy are being starved of capital. And the FCA has been given a new ‘consumer duty’ which is to ensure investors can make properly informed decisions about what investments to buy – but these charges disclosures misinform consumers, so that they cannot make a properly informed decision at all. All these areas of the FCA remit are being flouted by the current charges disclosure rules

As urgent action has not been taken by the FCA to change the reality for investors, it is time for Ministers to take the lead: The Government should ensure these charges rules do not misinform investors any longer. UK listed investment companies should be excluded from PRIIPs and MIFID rules that mislead investors, so that the FCA can uphold its consumer duty, undo market dislocations, revive capital markets and ensure international competitiveness for British companies, bringing us into line with the rest of the world, opening the way for investors to starting buying again.

2 thoughts on “Time for Ministers to intervene on Investment Trusts, as FCA has failed to achieve change”

I am wholly in agreement with this superb article. The entire investment company sector owes Ros a deep debt of gratitude for doggedly continuing to fight for these crucial changes to be made by the FCA.

The FCA is out of control, imposing new costs, the legal and accountancy firms being huge beneficiaries. They coupled with other regulators have made the UK un-invest-able, that is what they say on CNBC and Bloomberg interviews. Hence the valuations, which can be seen as a proxy for the cost of their actions.